I’ve been meaning to sign up to ClearScore for a while now, ever since I saw a TV advert for them; ‘giving everybody access to their credit score and report for free, forever.’

I’ve been quite open in the past about our past issues with debt, and how we’ve worked incredibly hard to take back control and sort them. Having done it once, we’ll never let it happen again, and one of the biggest tools in that fight is a credit report. Knowing what is on it, what your credit score is, what factors are affecting it right now – they’re all so important.

But of course,you usually have to pay for that – so naturally pricked up my ears when I saw that clearScore claim you can have access to it free, forever.

So when I got asked to take a look at the new ‘Coaching’ feature that ClearScore has launched I took it as A Sign, and immediately logged myself in to take a look. And honestly? I’m oh-so-impressed.

Firstly, I have to say I love the fresh open feel of the ClearScore site – not at all seriously intimidating or confusing. Everything’s laid out clearly in a bright, fresh design that anyone can understand; immediately you feel like you’ve taken a breath of fresh air and are starting to be in control. So having had a quick scooch around my credit score (which is drawn from Equifax, so why you’d ever go pay Equifax for it I’m not sure…) I headed straight into the Coaching.

This is the start of the coaching ‘chat’ – not a live person, but automated bot comments laid out like a conversation. It’s a simple, conversational way of communicating, and I’m guessing the script changes depending on which of the pre-set answers you select.

ClearScore Coaching

We started off with a general conversation about money – which is a great place to begin. I know a lot of debt issues are caused by people who simply hide form them – ignoring the problem and hoping it goes away never ends well, and yet time and again I see people trying it.

Once we’d worked through the basics, we started on the practical stuff. I think I’ pretty knowledgeable about the basics of credit and debt control (having learned what i needed the hard way!) so I didn’t really expect this part to be of any use to me. Wrong immediately! Obviously the information covered a lot of the basics…

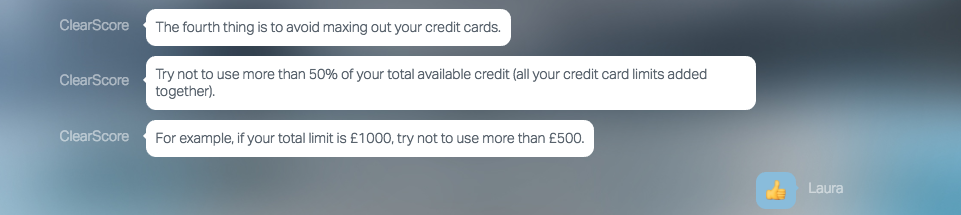

But there were some really useful gems in there too. For instance, while I knew that using ALL of the credit available to you was never good, making it look like you max out everything you can, I didn’t realise that there were actual set parameters to this;

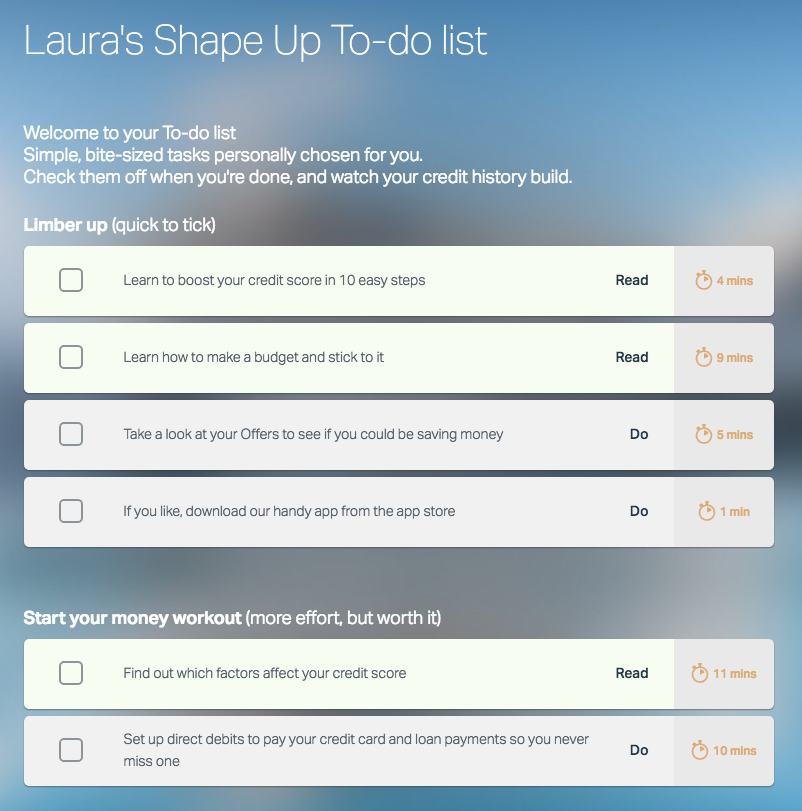

Once I’d worked through the Shape up Coaching Plan (which took me maybe ten minutes, with a break in the middle to go and make coffee; don’t worry, the system remembers where you got to and you don’t have to start all over again if you abandon it half way through), I was left with a personalised task plan.

And come on – who doesn’t love a To Do list?

Clicking on each of these tasks takes you off to a different page on the ClearScore site, which you know I’d relevant to your situation and is full of more in depth info than the original coaching plan. For instance the ‘factors affecting your credit score’ page had a lot more info on the effects on your credit score by that ratio of borrowing I mentioned just now:

Equifax have created the following traffic light system as a guide to show how credit utilisation might impact your credit score:-

- If you use less than 50% of your total credit limit, it shouldn’t have a negative impact on your credit score (‘green flag’)

- If you use between 50% – 75% of your total credit limit, this will show up as an ‘amber flag’ on your credit report, meaning it may have an effect on your credit score

- If you are using more than 75% of your total credit limit, this will be a ‘red flag’ on your credit report, and it’s likely to have a negative effect on your credit score.

This means, ideally, you should think about carefully managing your credit utilisation. So for example, if you total limit is £1000, you might not want to use more than £500. If you have multiple cards or accounts, you might want to share out the amount you’re borrowing across the cards, rather than maxing out one card (but only if this makes financial sense).

So – did I find the coaching useful? D’you know what, I did. Firstly, it is ALWAYS a good thing to have a very clear understanding of your financial situation. No matter how dire it might feel, having every detail clearly laid out is the very first step in taking control. I know the first time I did it, a weight I hadn’t even know existed was lifted from my brain. Looking at it in black and white allowed me to focus, to organise – and to feel like it wasn’t all whizzing out of control around my head.

I took away some really useful tips – and I’m certain that a few years ago, when I was incredibly ignorant of all things credit/debt related it would have been even more so. I love the site, I love the ClearScore app – which is now happily on my phone – and best of all, I love that it is all free. If you’re worrying about your debt, or thinking about organising your current credit, then head over there and start getting yourself organised. There’s simple step-by-step guides, with cyber hand holding and information aplenty. And that can only be a good thing.

12 June 2018

How do I apply for a credit to pay off a debit of £3000

14 June 2018

Lorraine if you apply for credit to pay off a debt, then you’re not actually paying off the debt, simply transferring it. I suggest a read of this may possibly help you – https://www.moneysavingexpert.com/loans/debt-help-plan